How much does liability insurance cost for a contractor? This ain’t rocket science, but it’s crucial for any builder, plumber, or landscaper. Different jobs, biz sizes, and locations all impact the price. Plus, your claims history is a major factor. Knowing the ins and outs of policies and how to compare quotes is key to saving cash.

We’ll delve into everything from general liability to pro liability, plus strategies for slashing costs.

Understanding the nuances of contractor liability insurance can be a real headache. But this guide breaks down the complexities into digestible chunks. We’ll explore the key factors that influence pricing, from the type of work to the contractor’s experience level. You’ll get the lowdown on different types of coverage and how to compare quotes effectively. We’ll even highlight some tricks for saving money on premiums, without compromising coverage.

Factors Affecting Contractor Liability Insurance Costs

Contractor liability insurance protects businesses from financial losses stemming from claims of injuries or property damage caused by their work. Understanding the factors influencing these costs is crucial for contractors to secure appropriate coverage at competitive rates. Insurance premiums are not a fixed amount; they vary significantly based on numerous elements.

Types of Work Performed

Different types of construction work carry varying levels of risk. High-risk activities, such as working at heights or with hazardous materials, typically result in higher premiums. Residential projects, while generally considered lower risk, can still incur costs depending on the complexity and scale of the project. Commercial projects, with their potential for larger-scale damage and more complex structures, usually command higher insurance premiums.

Specialized work, like demolition or excavation, often demands higher coverage limits and premiums to reflect the greater potential for severe accidents or damage.

Size of the Business

The size of a contracting business is a key factor in determining liability insurance costs. Smaller operations, often with fewer employees and less complex projects, may have lower premiums compared to larger companies with numerous projects and extensive teams. The number of employees, the scope of operations, and the total annual revenue all contribute to the risk assessment and subsequently, the premium calculation.

Location of the Business

Geographic location plays a substantial role in insurance costs. Areas with higher incidences of natural disasters, severe weather events, or accidents may have higher insurance premiums. Proximity to densely populated areas or high-value properties can also influence costs. Insurance companies consider local factors like construction regulations, labor laws, and accident rates when setting premiums.

Contractor’s Experience Level

Insurance companies often assess a contractor’s experience and track record when determining premiums. New contractors with limited experience are generally viewed as higher risk, leading to higher premiums. Established contractors with a proven track record of safe operations and successful project completions often qualify for lower premiums. A contractor’s experience directly impacts the insurance company’s assessment of the potential for accidents and claims.

Claims History

A contractor’s claims history is a critical factor in determining their insurance premiums. A history of accidents or claims increases the perceived risk, resulting in higher premiums. Conversely, a clean claims history signals a lower risk and can lead to lower premiums. Insurance companies analyze prior claims, including their severity and frequency, to determine the contractor’s risk profile.

Claims history is often the most influential factor in adjusting premiums over time.

Methods for Calculating Costs

Various methods are used to calculate contractor liability insurance costs. These include actuarial models, which utilize statistical data on past claims to predict future risk. Insurers also consider factors like the type of work performed, the contractor’s experience, the location of the business, and the size of the operation. The use of risk assessment tools helps insurers determine the appropriate coverage and premiums for each contractor.

These models and calculations often include a component for the amount of potential liability.

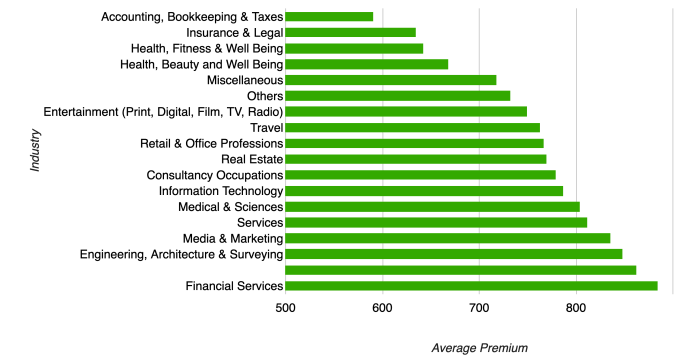

Typical Cost Differences by Contractor Type

| Contractor Type | Typical Cost Differences |

|---|---|

| Residential | Generally lower premiums due to lower risk profile and smaller-scale projects. |

| Commercial | Higher premiums due to greater potential for larger-scale damage and complex projects. |

| General | Premiums can vary depending on the specific work performed and the size of the operation. A broad range of potential risks is inherent in general contracting. |

Types of Contractor Liability Insurance

Protecting a construction business from potential financial losses is crucial. Various liability insurance types safeguard contractors against unforeseen events, ensuring business continuity and peace of mind. Understanding the different types and their coverage is essential for making informed decisions.

Different Types of Liability Insurance

Contractors face diverse risks, requiring a tailored approach to insurance. Different policies address specific liabilities, providing varying levels of protection. General liability, professional liability, and workers’ compensation are key types.

General Liability Insurance

This type of insurance safeguards contractors against claims arising from accidents or property damage during work. It covers injuries to third parties, damage to their property, and lawsuits stemming from negligence. Typical coverage amounts for general liability vary, but a common range is between $1 million and $5 million per incident. A contractor working on a large project might require a higher coverage amount than a small-scale contractor.

For instance, a contractor building a high-rise apartment complex is likely to have a much higher coverage requirement compared to a contractor performing minor renovations.

Professional Liability (Errors and Omissions) Insurance

This insurance type protects contractors against claims arising from professional mistakes, errors, or omissions in their work. It covers legal fees and settlements if a client sues due to the contractor’s negligence or failure to meet professional standards. The coverage amount for professional liability is typically determined based on the contractor’s work, industry standards, and potential liabilities. The amount varies significantly depending on the nature of the project and the contractor’s experience.

A contractor handling complex engineering projects would likely require a higher coverage limit than a contractor performing simpler tasks.

Workers’ Compensation Insurance, How much does liability insurance cost for a contractor

This type of insurance covers medical expenses and lost wages for employees injured on the job. It protects the contractor from financial liability related to workplace injuries. The coverage amount depends on the number of employees and the potential for injuries. For instance, a construction company with many employees working at high altitudes would require a higher workers’ compensation coverage than a company with only a few employees working in a low-risk environment.

The coverage amount is generally calculated based on state regulations and the number of employees. A company with a larger workforce will face higher premiums than a smaller company.

Coverage Comparison Table

| Insurance Type | Essential Coverages | Examples of Covered Situations | Examples of Uncovered Situations |

|---|---|---|---|

| General Liability | Bodily injury liability, property damage liability, advertising injury | Customer slips and falls on the worksite, damage to a neighboring property during construction | Intentional acts, damage caused by faulty materials provided by the contractor |

| Professional Liability (Errors & Omissions) | Errors, omissions, negligent acts, professional mistakes | Incorrect design plans leading to structural issues, failure to meet contractual obligations | Damage caused by faulty materials provided by the client, issues arising from external factors like weather |

| Workers’ Compensation | Medical expenses, lost wages, rehabilitation costs | Employee injuries sustained during work, treatment costs, temporary or permanent disability | Injuries sustained off-site, injuries caused by the employee’s deliberate actions |

Contractor Insurance Quotes and Comparison

Securing the right liability insurance is crucial for contractors. Comparing quotes from various providers allows you to find the best coverage at the most competitive price. Understanding the nuances of different policies is key to making an informed decision that protects your business and your bottom line.Comparing contractor liability insurance quotes is a multi-faceted process that requires careful evaluation of various factors.

A structured approach will ensure you select a policy that meets your specific needs and budget while providing adequate protection. This involves understanding the different policy components, including deductibles, policy limits, and premiums, and how they all contribute to the total cost.

Structured Method for Comparing Quotes

A structured approach to comparing quotes involves systematically evaluating different policies from various insurance providers. Start by gathering quotes from multiple reputable insurers. This ensures a broader range of options and competitive pricing. Crucially, compare policies that cover similar risks and services.

Key Elements to Evaluate in Quotes

Evaluating contractor liability insurance quotes requires a meticulous review of key elements. A well-organized table is useful to track and compare these aspects:

| Element | Description | Importance |

|---|---|---|

| Deductibles | The amount you pay out-of-pocket before insurance coverage kicks in. | Lower deductibles typically mean lower premiums, but higher out-of-pocket expenses in case of a claim. |

| Policy Limits | The maximum amount the insurance company will pay for a claim. | Higher limits provide greater protection, but also increase premiums. Consider the potential risks associated with your projects. |

| Premiums | The regular monthly or annual payment for the insurance policy. | Premiums should be considered in the context of the coverage provided and the overall value it offers. |

| Coverage Types | Specific types of risks covered (e.g., property damage, bodily injury). | Thoroughly review the coverage types to ensure they align with your business’s specific activities and potential risks. |

| Exclusions | Specific situations or circumstances that are not covered by the policy. | Carefully review the exclusions to avoid surprises or gaps in coverage. |

Comparing Total Cost of Different Policies

Beyond individual elements, comparing the total cost of different policies is crucial. A policy with a lower premium might have a higher deductible or lower coverage limits. Calculate the total cost of the policy, including premiums, deductibles, and potential claim expenses. An example would be comparing a policy with a low premium but a high deductible to a policy with a higher premium but a lower deductible.

Evaluating Coverage Details of Different Policies

Understanding the specific coverage details is vital. Different policies offer varying degrees of coverage for different types of risks. For example, a policy might cover property damage, but exclude damage caused by faulty workmanship. Compare the details to ensure the policy adequately protects your business. It is important to ensure that the policy covers all potential risks associated with your line of work, such as liability for faulty materials, design flaws, or improper execution of work.

Strategies for Reducing Contractor Liability Insurance Costs

Reducing liability insurance premiums is a key concern for contractors. Effective risk management plays a crucial role in achieving this goal. By proactively identifying and mitigating potential risks, contractors can demonstrate a lower likelihood of claims, ultimately leading to more favorable insurance rates.

Figuring out how much liability insurance costs for a contractor can be tricky, like trying to sort through all the different weapons in Ratchet and Clank: Rift Apart. Ratchet and Clank Rift Apart weapons each have unique stats, and similarly, insurance premiums vary based on your specific needs and risks. Ultimately, you’ll need to get quotes to see the real price tag, just like you’d need to test out different weapons before tackling a tough foe.

So, do your research and compare policies before you choose your coverage.

Risk Management Practices for Contractors

Proactive risk management is paramount for contractors. This involves a multifaceted approach that goes beyond simply adhering to safety regulations. It requires a thorough understanding of potential hazards, implementing robust safety protocols, and continuously evaluating and improving these practices. A strong safety culture, coupled with regular training and clear communication, fosters a work environment that minimizes accidents and incidents.

Risk Assessments and Their Impact on Insurance Costs

Thorough risk assessments are critical in identifying potential liabilities. These assessments should encompass all aspects of the project, from the nature of the work to the working conditions and the site environment. Detailed assessments, analyzing potential hazards and outlining preventive measures, provide concrete evidence of a contractor’s commitment to safety. A well-documented risk assessment can directly influence an insurer’s perception of risk, potentially leading to lower premiums.

For instance, a contractor demonstrating a proactive approach to site safety through documented risk assessments might receive a more favorable insurance rate compared to one with a less comprehensive risk management plan.

Methods to Reduce Claims Frequency and Severity

Minimizing the frequency and severity of claims is essential for cost reduction. Implementing rigorous safety protocols, including regular safety inspections, equipment maintenance, and employee training, can significantly decrease the likelihood of accidents. Enforcing strict adherence to safety guidelines and protocols across all project phases is vital. Furthermore, contractors should have a clear incident reporting system, enabling prompt responses to any safety issues and minimizing potential damage.

This includes well-defined procedures for addressing and resolving incidents promptly, aiming to limit their impact and prevent escalation.

Figuring out how much liability insurance costs for a contractor can be tricky, right? But did you know that a busted AC unit could be a whole different ballgame? If your AC conks out, learning how to get your home warranty to replace it here could save you a bundle. Ultimately, though, contractor liability insurance rates depend on factors like your experience level and the type of work you do, making it a bit of a puzzle.

Table: Risk Mitigation Strategies and Potential Impact on Insurance Premiums

| Risk Mitigation Strategy | Potential Impact on Insurance Premiums |

|---|---|

| Comprehensive Risk Assessment | Potentially lower premiums due to demonstrable proactive risk management. |

| Regular Safety Inspections | Reduced claims frequency and severity, leading to lower premiums. |

| Employee Training and Competency | Improved adherence to safety procedures, lowering the likelihood of accidents and potential claims. |

| Strict Adherence to Safety Regulations | Lower premiums due to a proven commitment to safety standards. |

| Incident Reporting and Management System | Reduced claim severity and faster resolution, potentially leading to lower premiums. |

| Equipment Maintenance and Inspection | Reduced risk of equipment-related accidents and damages, resulting in fewer claims and lower premiums. |

Coverage Exclusions and Limitations

Contractor liability insurance, while offering crucial protection, doesn’t cover every potential mishap. Understanding the exclusions and limitations in your policy is vital to accurately assessing your risk and avoiding costly surprises. Knowing what’s not covered helps you proactively manage your business and make informed decisions.

Common Exclusions

Contractor liability insurance policies typically exclude coverage for certain types of claims. These exclusions are designed to prevent coverage for risks that are either inherently too broad, or are better addressed by other types of insurance. Understanding these exclusions is crucial for managing potential financial liabilities.

- Pre-existing Conditions: Coverage often excludes pre-existing conditions on a property or site. This means if a problem exists before your work begins, and your work inadvertently exacerbates or reveals the issue, you might not be covered. For instance, if a contractor uncovers structural damage during a renovation project, which was already present but not immediately apparent, their liability insurance might not cover the cost of repair if the damage was pre-existing.

- Work Performed Outside the Policy’s Scope: Insurance policies often have limitations on the types of work covered. If your work deviates significantly from the agreed-upon scope, coverage might be denied. A contractor hired to install windows might not be covered if they decide to perform additional work, such as drywall repairs, that falls outside their initial contract. The additional work, if resulting in a claim, might not be covered by their liability insurance.

- Intentional Acts or Fraud: Policies typically exclude coverage for damages or injuries resulting from intentional acts or fraud on the part of the contractor. If a contractor knowingly damages property or causes injury, their liability insurance would likely not cover the resulting claims. For example, a contractor who deliberately misrepresents materials used in a project would not be covered if a client suffers financial loss due to the misrepresentation.

- War or Terrorism: Losses or damages resulting from acts of war or terrorism are usually excluded. If a contractor’s work site is damaged or disrupted due to a terrorist attack, the insurance may not cover the losses.

Examples of Limited or Denied Coverage

Understanding when coverage might be limited or denied requires careful review of the specific policy details. Here are some examples:

- Bodily Injury Caused by Employee Negligence: While contractor liability insurance generally covers injuries to third parties, it might not cover injuries to employees of the contractor. A contractor’s worker’s compensation insurance would typically cover employee injuries.

- Property Damage Caused by a Defective Product: If the damage stems from a defective product supplied by a third party, the coverage might not extend to the contractor’s liability. A contractor installing appliances might not be covered if a defective appliance causes damage.

- Damage Resulting from Inadequate Supervision: If a contractor fails to properly supervise their employees, leading to damage or injury, coverage might be limited or denied. If a contractor’s employee causes damage due to lack of supervision, the liability insurance might not cover the resulting claim.

Coverage Exclusions Table

This table summarizes common exclusions and limitations in contractor liability insurance policies.

| Exclusion Category | Description | Example |

|---|---|---|

| Pre-existing Conditions | Problems present before work begins | Structural damage hidden beneath flooring |

| Work Outside Scope | Tasks beyond the agreed-upon contract | Contractor performing additional work not included in the initial agreement |

| Intentional Acts | Deliberate acts causing harm | Contractor intentionally damaging property |

| War or Terrorism | Damage from war or terrorist acts | Project site damaged during a terrorist attack |

What’s Not Covered

A typical contractor liability insurance policy does not cover all potential risks. Reviewing the specific policy details is crucial to understand the scope of coverage and identify potential gaps. This helps prevent costly surprises in the event of a claim.

Recent Trends in Contractor Liability Insurance

The landscape of contractor liability insurance is constantly evolving, mirroring shifts in the construction industry and broader economic factors. Understanding these trends is crucial for contractors to make informed decisions about their insurance needs and proactively manage potential risks. This dynamic environment necessitates a continuous assessment of coverage adequacy and cost-effectiveness.

Pricing Fluctuations

Contractor liability insurance premiums are influenced by a complex interplay of factors. Inflationary pressures, particularly in material and labor costs, are a significant driver of premium increases. Furthermore, rising interest rates often lead to higher borrowing costs for contractors, impacting their profitability and potentially influencing their ability to secure favorable insurance rates. The increasing frequency and severity of severe weather events, including hurricanes, floods, and wildfires, also contribute to premium adjustments.

The costs associated with repairing or mitigating damage from these events are often passed on to policyholders.

Impact of Construction Industry Changes

The construction industry itself is undergoing significant transformations. The growing prevalence of complex projects, often involving intricate designs and specialized technologies, necessitates higher levels of expertise and specialized insurance coverage. Increased use of technology, including automation and digital tools, brings both opportunities and new risks that insurance providers must address. These technological advancements can sometimes lead to unforeseen issues or vulnerabilities in project execution, which are reflected in premiums.

Furthermore, the increasing demand for sustainable construction practices, while environmentally beneficial, can also introduce new layers of complexity and potential liabilities, affecting insurance costs.

Legislative and Regulatory Updates

Recent legislative and regulatory changes also play a crucial role in shaping contractor liability insurance costs. For example, stricter environmental regulations, including stricter waste disposal and hazardous material handling protocols, necessitate increased insurance coverage for potential environmental liabilities. Changes in labor laws and regulations related to worker safety and compensation also impact insurance costs. Modifications to building codes and safety standards, such as those related to earthquake-resistant designs or fire prevention measures, are examples of regulations that influence insurance premiums.

Emerging Risks and their Impact

The construction industry faces emerging risks that are challenging the traditional approach to insurance. Cybersecurity threats are increasingly relevant as construction projects rely more on digital systems and data. The potential for data breaches or system failures can lead to substantial financial losses and increased liability for contractors. Furthermore, the growing prevalence of remote work and virtual collaboration within the construction sector introduces new challenges related to insurance coverage and risk management.

These emerging risks are a significant consideration for insurers and necessitate innovative solutions in insurance products and pricing structures. A recent example includes the growing use of drones in construction, which introduces liability concerns for incidents involving property damage or personal injury.

Conclusion

So, there you have it – a comprehensive look at contractor liability insurance costs. From the various factors affecting pricing to strategies for reducing premiums, this guide equips you with the knowledge to make informed decisions. Remember, insurance is a vital investment for protecting your business and peace of mind. Comparing quotes and understanding the nuances of different policies is paramount to finding the best deal without compromising essential coverage.

Popular Questions: How Much Does Liability Insurance Cost For A Contractor

What are common exclusions in contractor liability insurance policies?

Typical exclusions include work performed outside the policy’s geographical limits, intentional acts of wrongdoing, or pre-existing damage to the property. Check the fine print carefully!

How does the size of my business affect insurance costs?

Larger businesses often face higher premiums due to the potential for larger claims. Factors like the number of employees and the scope of operations are considered. Small businesses usually have lower premiums, but it’s still important to shop around.

What’s the difference between general liability and professional liability insurance?

General liability covers claims arising from bodily injury or property damage caused by your work. Professional liability (Errors & Omissions) protects you from claims related to mistakes or omissions in your professional services.

How can I get a better quote?

Shop around for quotes from different insurers, compare coverages and premiums, and consider increasing your deductibles. Having a strong risk management plan will improve your chances of getting a favorable quote.